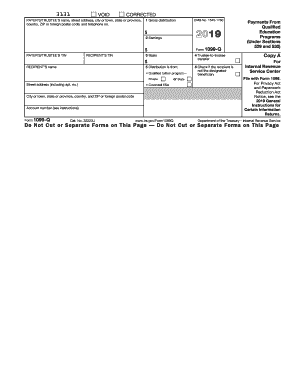

IRS 1099-Q 2025-2026 free printable template

Get, Create, Make, and Sign IRS 1099-Q

Instructions and Help about IRS 1099-Q

How to edit IRS 1099-Q

How to fill out IRS 1099-Q

Latest updates to IRS 1099-Q

All You Need to Know About IRS 1099-Q

What is IRS 1099-Q?

Who needs the form?

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about IRS 1099-Q

What should I do if I realize I've made an error on my IRS 1099-Q after filing?

If you notice an error on your IRS 1099-Q after submission, you should file a corrected version as soon as possible. Utilize IRS Form 1099-Q Corrected to amend the mistake, ensuring that you clearly indicate the changes made. It's crucial to keep a copy of both the original and corrected forms for your records.

How can I verify if my filed IRS 1099-Q has been received by the IRS?

To check the status of your filed IRS 1099-Q, you can use the IRS's e-file tracking system or contact the IRS directly. Keep in mind that processing times may vary, and it's advisable to wait a few weeks before checking to ensure your form has been adequately processed.

What steps should I take if I received an IRS notice regarding my 1099-Q?

Upon receiving an IRS notice related to your 1099-Q, carefully read the communication to understand the issue. Gather any necessary documentation to support your case and respond promptly, addressing the concerns raised in the notice to avoid potential penalties or further complications.

Are there specific fees associated with e-filing my IRS 1099-Q?

Yes, some e-filing services may charge a fee for filing your IRS 1099-Q electronically. It's recommended to research various e-filing options to find one that fits your needs. Be aware of refund policies in case your submission is rejected.

What common errors should I be aware of to avoid when filing an IRS 1099-Q?

Common errors when filing an IRS 1099-Q include incorrect taxpayer identification numbers, misspellings of names, and inaccurate dollar amounts. Carefully review all information before submission, and consider using tax software that can help minimize such mistakes.